Eurozone Crisis and Banks' Creditworthiness: What is New for Credit Default Swap Spread Determinants? - Alessandra Ortolano, Eliana Angelini, 2022

Por um escritor misterioso

Descrição

Balance sheet structure of an individual bank

Risks, Free Full-Text

Risks Special Issue : Credit Risk Management

UML class diagram of the proposed model. The proposed model consists of

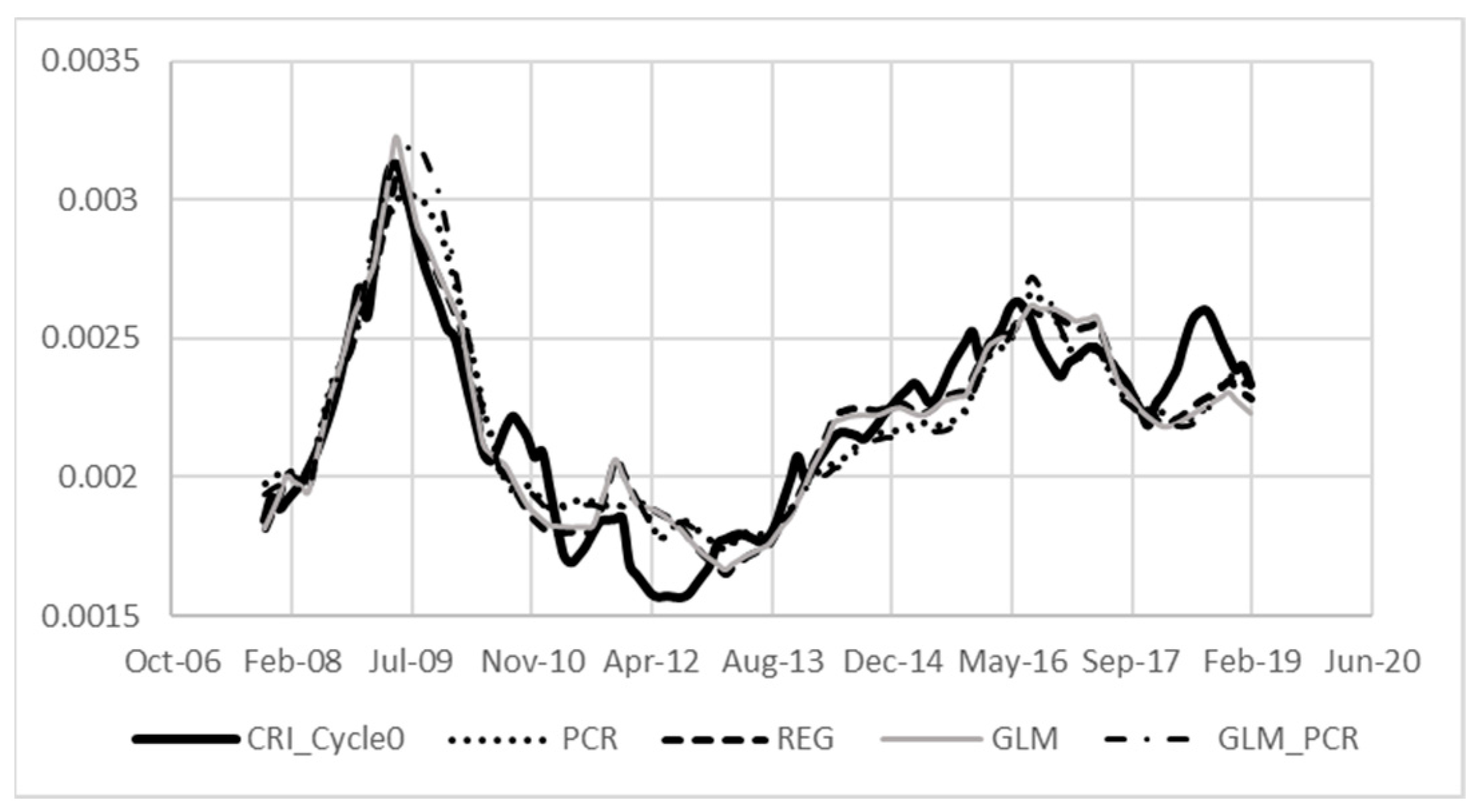

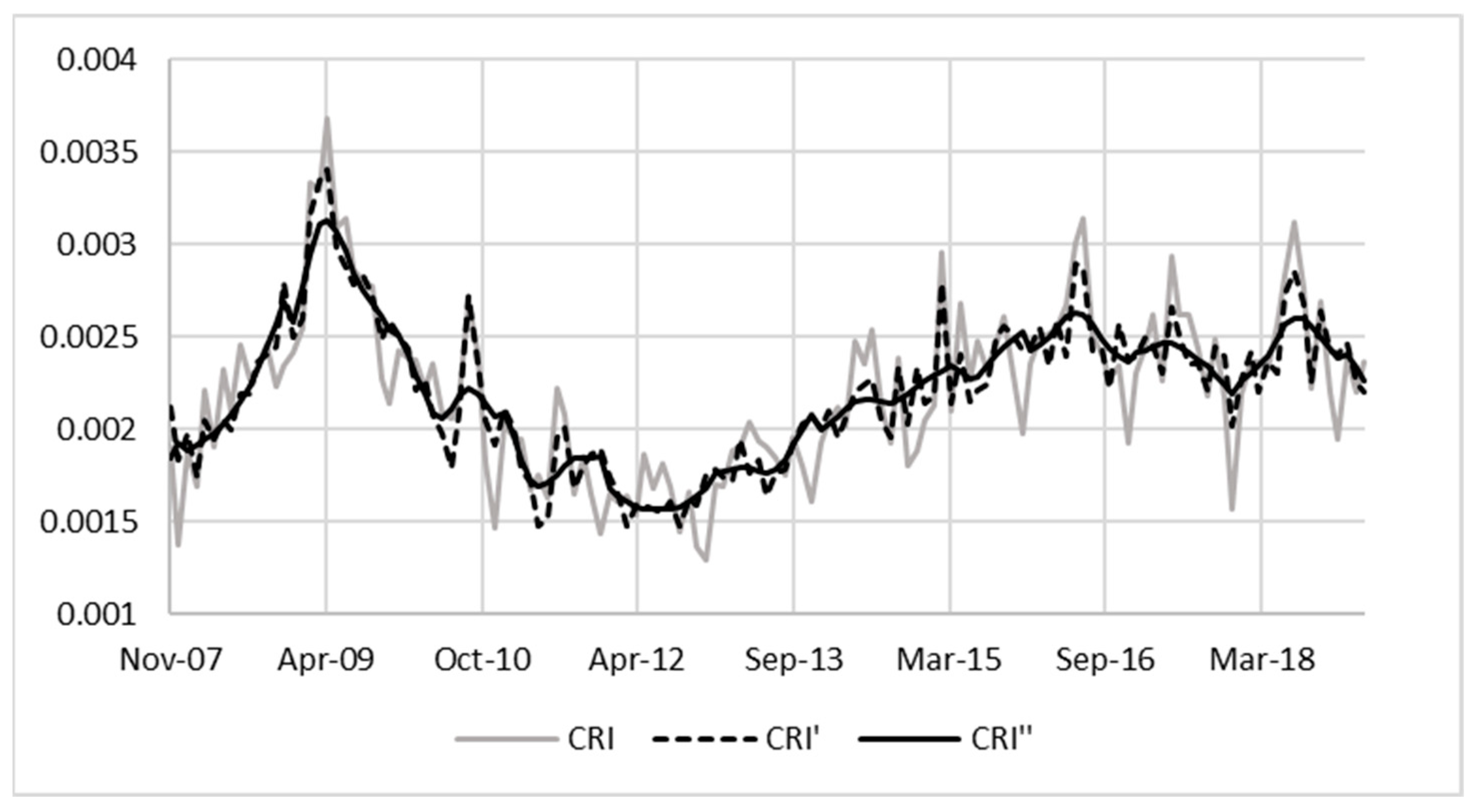

Selected Eurozone sovereign spreads (five-year credit default swap

PDF) Fundamental determinants of credit default risk for European and American banks

Daily volatility of portfolio returns in the financial and economic

The auto-correlogram and square of returns in UK market

PDF) The Time-Spatial Dimension of Eurozone Banking Systemic Risk

The auto-correlogram and square of residuals in UK market based on the

PDF) Eurozone Crisis and Banks' Creditworthiness: What is New for Credit Default Swap Spread Determinants?

Risks, Free Full-Text

Alessandra ORTOLANO, Research Assistant, Tuscia University, Viterbo, Tuscia, Department of Economics, Engineering, Society and Business Organization - DEIM

de

por adulto (o preço varia de acordo com o tamanho do grupo)